See Our Latest Blogs

Lorem ipsum dolor sit amet, consectetur

Every Canadian InCorporated Person's Dilemma

Every Canadian InCorporated Person's Dilemma

How to Take Money (Retained Earnings) Out of Your Corporation Tax-Free Using Corporate-Owned Life Insurance (COLI)

As a small business owner or incorporated professional in Canada, you’re likely sitting on a growing pool of retained earnings inside your corporation. The question is: How do you access those funds efficiently—without triggering hefty taxes?

Enter Corporate-Owned Life Insurance (COLI): a powerful, often overlooked strategy to extract wealth from your corporation tax-free, protect your family or business, and build long-term financial security.

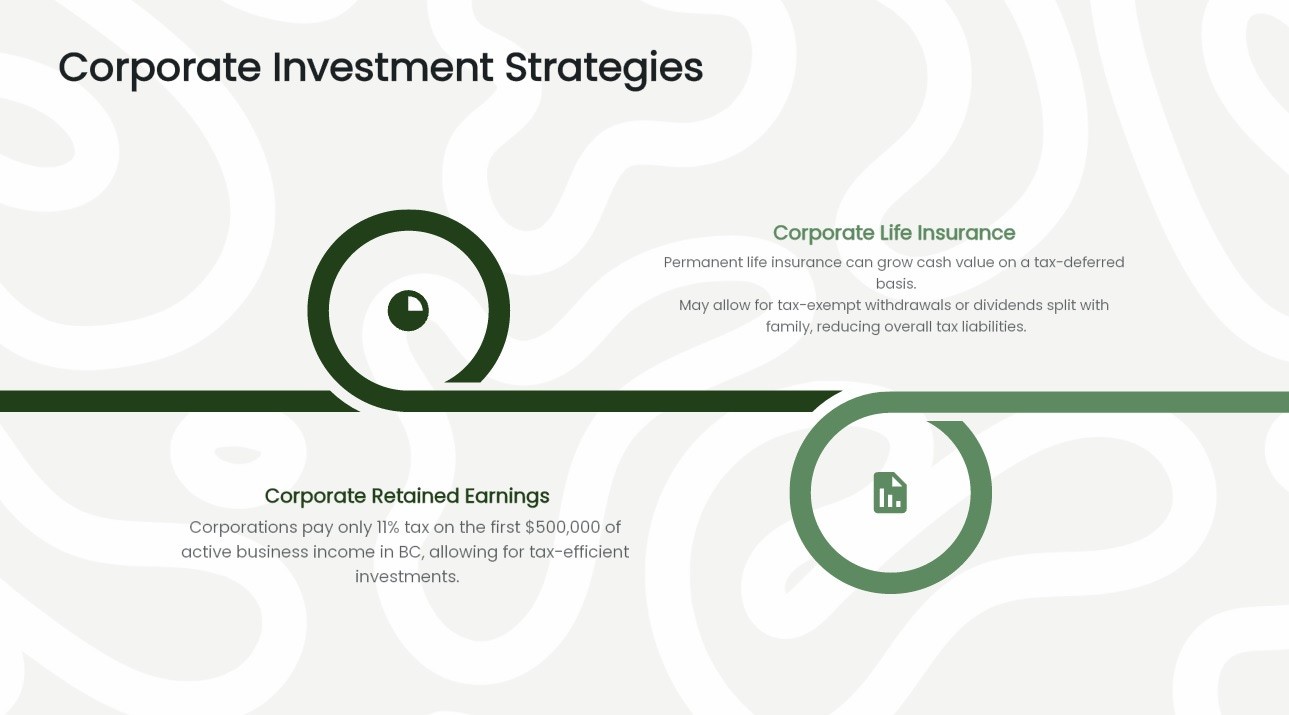

The Problem: Retained Earnings Are Trapped

Retained earnings are the after-tax profits your corporation holds onto rather than paying out as dividends or salaries. While they can be reinvested into the business, many owners accumulate them for future needs—retirement, succession planning, or simply wealth preservation.

But withdrawing those funds personally means facing:

Dividend tax, especially painful in high-income provinces.

Capital gains tax if you’re trying to sell the business.

Double taxation at death (once inside the corporation, again when paid out).

So, what if there were a way to convert those retained earnings into a personal, tax-free legacy?

The Solution: Corporate-Owned Participating Whole Life Insurance

Corporate-Owned Life Insurance (COLI), particularly Participating Whole Life Insurance, offers a unique combination of:

Permanent life insurance coverage,

A tax-sheltered investment component (cash value growth),

And a mechanism to extract retained earnings tax-free upon death through the Capital Dividend Account (CDA).

Here’s how it works.

How COLI Works Inside a Canadian Corporation

The Corporation is the Owner and Beneficiary

Your company pays the premiums using its retained earnings. The life insurance policy is corporately owned, and the company is the beneficiary.Premiums Come from Tax-Advantaged Dollars

Since corporate tax rates are lower than personal tax rates, paying premiums with corporate dollars (retained earnings) is far more efficient than using after-tax personal income.Cash Value Grows Tax-Sheltered

The investment portion of a Participating Whole Life policy grows inside the policy tax-free. This creates a growing pool of accessible funds, which can be collateralized for business or personal use.Death Benefit Pays to the Corporation

Upon your death, the insurance proceeds are paid out to the corporation. These proceeds—minus the adjusted cost basis—can be credited to the CDA.Tax-Free Distribution via the Capital Dividend Account

The CDA allows your corporation to distribute this amount tax-free to your estate or heirs. This bypasses double taxation and ensures your retained earnings exit the company without triggering personal taxes.

A Powerful Tool for Tax and Estate Planning

Beyond just tax efficiency, COLI provides:

Estate preservation: Ensures your heirs don’t have to sell business assets to cover tax liabilities.

Liquidity for succession: Business partners can use the death benefit to buy out your shares.

Wealth accumulation: The policy’s cash value can be accessed during your lifetime via policy loans or collateral loans.

Who Should Consider COLI?

Incorporated Professionals (Doctors, Dentists, Lawyers)

Owner-Operators of Small to Medium-Sized Businesses

Those with excess retained earnings not needed for operations

Anyone looking for a long-term tax-efficient retirement or estate plan

Things to Watch Out For

Premiums are not tax-deductible

Policies must be properly structured to qualify for CDA credit

Early cancellation may trigger tax on gains

Ensure professional collaboration between your accountant, insurance advisor, and legal team

Real-World Example

A professional corporation has $500,000 in retained earnings. Rather than investing in taxable GICs or paying out a dividend (taxable again), the corporation invests $50,000 annually into a Participating Whole Life Insurance policy.

Over 20 years:

The cash value accumulates tax-deferred.

At death, the policy pays out $1.5M to the corporation.

~$1.45M is credited to the Capital Dividend Account.

The corporation distributes $1.45M tax-free to the shareholder’s family.

That’s $1.45M extracted tax-free—a strategy that not only preserves wealth but enhances your legacy.

Conclusion

Corporate-Owned Life Insurance is not just an insurance product—it’s a strategic tax-planning vehicle for Canadian business owners who want to do more with their retained earnings.

Whether you're looking to minimize taxes, build a tax-sheltered legacy, or unlock your corporation’s wealth without giving half of it to the CRA, COLI might be the financial solution you didn’t know you needed.

👉 Get in touch with Consultant Manpreet or Talk to your accountant and/or a qualified insurance advisor today to see how COLI can fit into your corporate and estate plan.